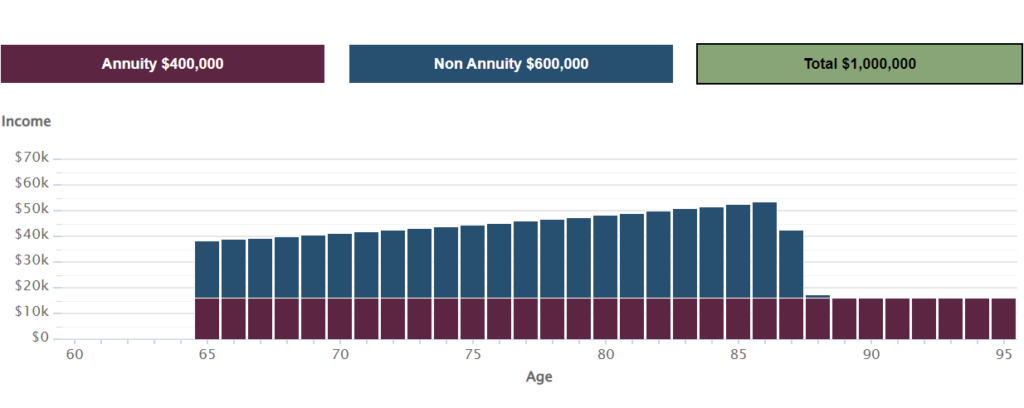

Annuity Withdrawal Strategies Maximizing Income while Preserving Principal in Annuity Portfolio Management and Asset Allocation In annuity portfolio management and asset allocation, understanding effective withdrawal strategies is crucial for maximizing income and preserving principal. Annuities provide a reliable source of income, and how withdrawals are structured can significantly impact long-term financial goals. Annuity Withdrawal In this comprehensive guide, we will explore various options for annuity withdrawals and income generation, as well as the associated penalties and limitations. Furthermore, we will examine strategies to help individuals optimize their income while preserving the underlying principal within their annuity portfolios. By employing the right withdrawal strategies, investors can enhance their financial security and make the most of their annuity investments.

Options for Annuity Withdrawals and Income Generation

- Fixed Period or Systematic Withdrawals: This withdrawal option allows individuals to receive regular payments over a predetermined period. It provides a consistent income stream, offering stability and budgeting convenience. Annuity Withdrawal

- Lifetime Income or Annuity Payouts: Lifetime income options ensure a steady stream of payments for the duration of an individual’s life, offering protection against longevity risk. These options include life-only, joint and survivor, and specific period annuity payouts.

- Systematic Withdrawals with Interest: This strategy involves withdrawing a fixed percentage of the annuity’s account value plus any interest earned. It allows for potential growth while providing regular income.

Understanding Withdrawal Penalties and Limitations

- Surrender Charges: Annuities often come with surrender charges incurred when withdrawals are made before a specific surrender period has passed. These charges typically decrease over time, encouraging investors to maintain their annuity contracts for the long term.

- Excess Withdrawal Penalties: Annuities may impose penalties for exceeding the allowable withdrawal limits within a given year. It is essential to be aware of these limits to avoid unnecessary penalties and ensure effective income planning. Annuity Withdrawal

- Tax Considerations: Withdrawals from annuities are subject to taxation based on the portion considered earnings or gains. Understanding the tax implications is vital when planning withdrawal strategies to optimize after-tax income. read more

Strategies to Maximize Income While Preserving Principal

- Assessing Income Needs and Goals: Determine your desired income level and financial objectives before structuring your withdrawal strategy. Consider factors such as living expenses, inflation, and desired lifestyles to set realistic income targets. Annuity Withdrawal

- Establishing a Sustainable Withdrawal Rate: Calculate a sustainable withdrawal rate that balances income needs with the preservation of principal. This rate considers life expectancy, investment returns, and risk tolerance factors.

- Utilizing Systematic Withdrawal Approaches: Systematic withdrawals, such as fixed percentage or fixed dollar amount withdrawals, provide a predictable income stream. Adjusting the withdrawal rate based on changing needs and market conditions can help balance income generation and principal preservation.

- Incorporating diversification in asset allocation: Diversifying annuity portfolios across different asset classes can help manage risk and optimize income. By spreading investments across equities, fixed income, and other suitable assets, individuals can increase overall returns and income streams.

- Consider Layering Annuities: Layering annuities involves staggering the purchase of multiple annuity contracts over time. This strategy allows for a more flexible approach to income planning, potentially taking advantage of higher payout rates in the future while maintaining immediate income needs.

- Taking Advantage of Optional Benefit Riders: Some annuities offer optional benefit riders, such as guaranteed minimum withdrawal benefits (GMWB) or lifetime withdrawal benefits (GLWB). These riders provide income guarantees while offering flexibility in withdrawal amounts.

- Regularly review and adjust the withdrawal strategy.

To ensure the ongoing effectiveness of your annuity withdrawal strategy, it is essential to review and make necessary adjustments regularly. Here are some considerations:

a. Market Conditions: Keep an eye on market trends and economic conditions that may affect your annuity portfolio. Adjusting your withdrawal strategy based on market performance can help maximize income while mitigating potential risks.

b. Rebalancing: Periodically rebalance your annuity portfolio to maintain the desired asset allocation. This ensures that your investments are aligned with your long-term goals and income needs.

c. Lifestyle Changes: Life events such as retirement, relocation, or changes in personal circumstances can impact your income requirements. Review your withdrawal strategy to accommodate these changes and ensure your annuity portfolio continues to meet your evolving needs.

d. Consultation with Financial Professionals: Seek advice from financial advisors or annuity specialists who can provide insights tailored to your situation. They can help you assess your withdrawal strategy, identify potential areas for optimization, and ensure that it aligns with your overall financial plan.

e. Consider Inflation Protection: Over time, inflation erodes the purchasing power of your income. Explore options for incorporating inflation protection into your annuity withdrawal strategy, such as inflation-adjusted annuities or investments that offer inflation-beating returns.

f. Estate Planning: Evaluate how your annuity withdrawal strategy aligns with your estate planning goals. Consider factors such as legacy planning, minimizing tax implications for heirs, and ensuring a smooth transition of your annuity assets.

Conclusion

Effectively managing annuity withdrawals is a critical aspect of portfolio management and asset allocation. By exploring various withdrawal options, understanding associated penalties and limitations, and implementing strategies to maximize income while preserving principal, investors can optimize their annuity portfolios for long-term financial security. Regularly reviewing and adjusting withdrawal strategies, considering market conditions, and seeking professional guidance is vital for ensuring the ongoing success of annuity withdrawals. By incorporating these approaches, individuals can make the most of their annuity investments, enjoy a consistent income stream, and protect their principal over time. Annuity Withdrawal

{kind=link}